Section 2: Full findings and recommendations

This section explores the results from our data-driven horizon scan into green technologies for decarbonising heating and mitigating climate change. Nesta is committed to supporting the transition of the country’s 29 million homes to sustainable heating, and this has guided our focus on low-carbon heating and energy efficiency technologies in this analysis.

We encourage you to interpret the results of this work as data-informed hypotheses about the research and innovation trends as opposed to comprehensive conclusions, given the limitations of our datasets and approach as described in Section 3.

Analysing signals from research

We tracked the trajectory of UK research activity around various green technologies, and evaluated it using our typology of trends. Figure 1 shows an example where we have used the average number of projects in the Gateway to Research (GtR) database across the past five years as the signal magnitude, whereas signal growth has been captured by a smoothed estimate of the relative change in the number of projects across the same time period.

When examining specific low carbon heating and energy efficiency and management technologies, we found marked differences in their research activity trends (Figures 2-3).

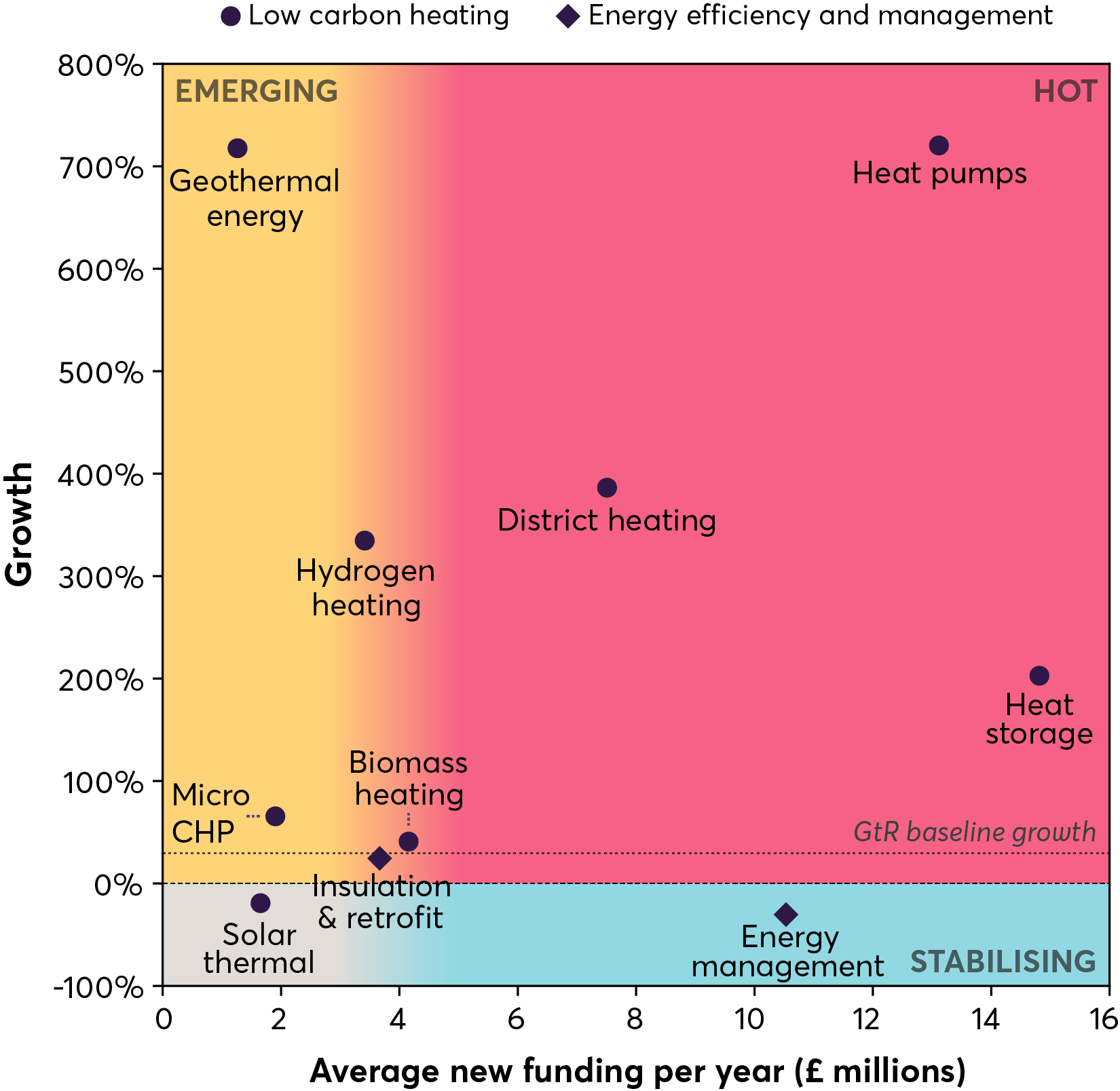

Research involving heat pumps and heat storage appears ‘hot’ according to our typology (meaning that the number of projects as well as the amount of funding are at a relatively high magnitude and high growth). Alongside research focused on improving the technology, such as improving the efficiency or reducing capital costs of heat pumps, in the past couple of years we have also seen projects receiving larger amounts of funding (with more than £3 million funding each) that are trialling heat pumps as one part of a scaled-up solution, often together with other technologies. This includes the ReFlex Orkney project involving heat pumps, hydrogen and heat storage and the London-based GreenSCIES project that uses heat networks and heat pumps to utilise waste heat from data centres and the London Underground.

We also see some recent examples of data-driven modelling of the thermal performance of buildings to predict energy savings from installing heat pumps (alongside other retrofitting measures) and support the novel ‘heat as a service’ type of business model.

Figure 2. Research funding trends for decarbonising heating. Average magnitude and growth between 2016 and 2020, based on analysis of the UKRI's Gateway to Research (GtR) portal data.

Figure 2. Research funding trends for decarbonising heating. Average magnitude and growth between 2016 and 2020, based on analysis of the UKRI's Gateway to Research (GtR) portal data.

Figure 2. Research funding trends for decarbonising heating. Average magnitude and growth between 2016 and 2020, based on analysis of the UKRI's Gateway to Research (GtR) portal data.

Figure 3. Research project trends for decarbonising heating. Average magnitude and growth of the number of new projects between 2016 and 2020, based on analysis of the UKRI's Gateway to Research (GtR) portal data.

Figure 3. Research project trends for decarbonising heating. Average magnitude and growth of the number of new projects between 2016 and 2020, based on analysis of the UKRI's Gateway to Research (GtR) portal data.

Closer to the emerging area of our typology, we find hydrogen heating and geothermal energy, which both show a smaller number of projects and comparatively less funding across the past five years but are exhibiting strong recent growth. In light of the government’s hydrogen strategy and new funding announcements, we would expect research into hydrogen heating to continue to grow. District heating appears to be transitioning between the emerging and hot categories. The growth of these technology categories is similar or above the overall growth rate of new funding and projects in the Gateway to Research database, indicating a strong performance.

Conversely, research signals for micro combined heat and power, solar thermal and biomass heating appear closer to dormant (lower magnitude and small or no growth).

Finally, research on energy efficiency (insulation and retrofitting) and energy management measures (including smart home technologies and smart meters, as well as demand response and load shifting solutions) is at a relatively high magnitude but lower growth – indicative of stabilising dynamics.

These research trends appear broadly aligned with the expected contribution that the different technologies can make to the heat decarbonisation, as set out by the Climate Change Committee’s roadmap. Their plan primarily emphasises the contribution of heat pumps and heat networks, with less weight assigned to biomass or solar thermal, and hydrogen contribution being subject to sufficient production capacity.

Figure 3. Research project trends for decarbonising heating. Average magnitude and growth of the number of new projects between 2016 and 2020, based on analysis of the UKRI's Gateway to Research (GtR) portal data.

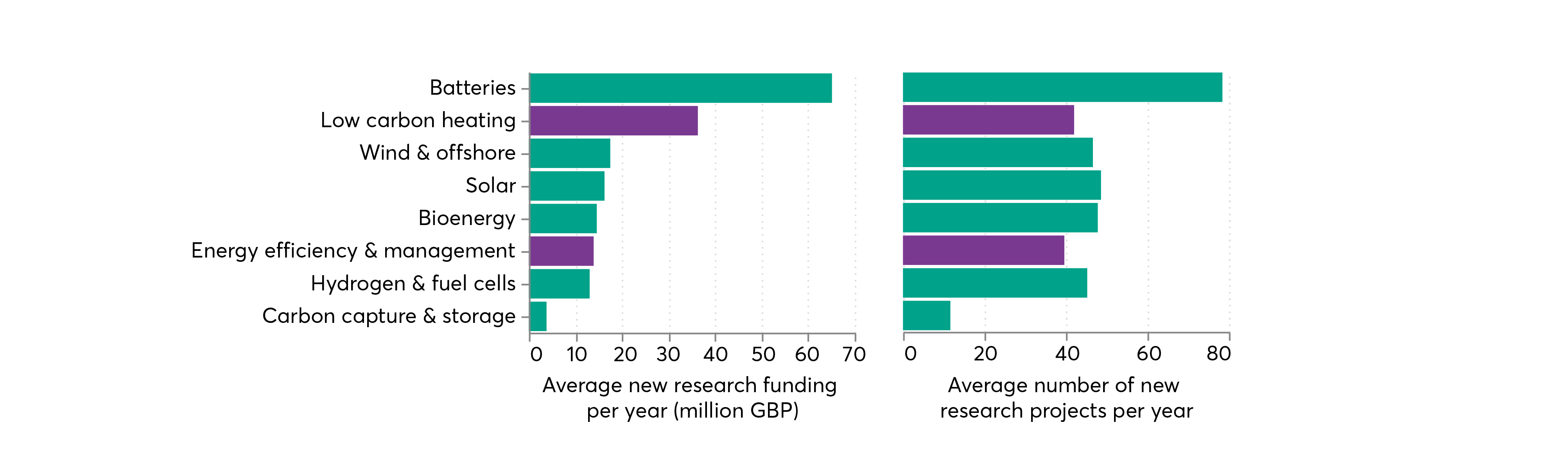

Importantly, when analysing the broader technology categories of low-carbon heating and energy efficiency and management, we find their research activity level and growth comparable to other established green technologies such as solar, wind and offshore, bioenergy or hydrogen and fuel cells (approximately 40-50 new projects per year on average; Figure 4).

In terms of funding, low-carbon heating appears to surpass most of these green technologies by approximately a factor of two (on average about £36 million vs £15 million in newly awarded funding per year). Among the technologies we examined, only batteries exhibited even higher levels and growth of funding amount, which is likely related to recent government initiatives which emphasise the importance of this technology (for example, the Faraday Battery Challenge announced in 2017).

Figure 4. UK research funding for green technologies. Estimated average figures between 2016 and 2020, based on analysis of the UKRI's Gateway to Research portal data.

Figure 4. UK research funding for green technologies. Estimated average figures between 2016 and 2020, based on analysis of the UKRI's Gateway to Research portal data.

Is business investment following research?

When promising innovations mature and transition from the stage of research and development to commercialisation and scaling, we would expect to find increasingly stronger venture capital investment signals.

Missing investment in low carbon heating?

Overall, we found a relatively low level of investment into businesses related to low-carbon heating technologies (Figures 5-6). The number of investment deals has stagnated since 2016, with around five deals per year. The average total yearly investment between 2016 and 2020 was around £15 million (the median deal being around £2 million). These figures are comparable to emerging technologies like hydrogen and fuel cells, and carbon capture and storage, which have recently exhibited strong growth and caught up with low-carbon heating.

Notable recent investments in businesses working on heating technologies include heat battery company Sunamp (several grants and series A deals between £300,000 in 2018 and £4.5 million in 2020), solar thermal company Naked Energy (£5.25 million in 2019), and ITM Power, which builds hydrogen electrolysers that can be joined up with the gas grid (£38 million in 2019). For companies that have mentioned heat pumps in their description, we found only a few deals in the past five years; for example, heat pump manufacturer Kensa (2020, undisclosed amount), Mixergy, whose heat tanks allow better utilisation of solar thermal and heat pumps (£3.6 million in 2019), and builder Verto Homes, which integrates heat pumps into smart houses (£1.4 million in 2016).

We note that we also identified a number of companies related to heating whose business description, however, was not sufficiently informative to determine whether they specialise in low-carbon heating. These companies are shown in Figures 5-6 as Heating (other) and they also exhibited a low level of investment.

Figure 5. Investment deals in green technologies. Average magnitude and growth between 2016 and 2020 based on analysis of Crunchbase data. Crunchbase baseline growth characterises the growth across all UK businesses in the database in the same time period.

Figure 5. Investment deals in green technologies. Average magnitude and growth between 2016 and 2020 based on analysis of Crunchbase data. Crunchbase baseline growth characterises the growth across all UK businesses in the database in the same time period.

Figure 5. Investment deals in green technologies. Average magnitude and growth between 2016 and 2020 based on analysis of Crunchbase data. Crunchbase baseline growth characterises the growth across all UK businesses in the database in the same time period.

Strong signals of investment in energy efficiency and management

In contrast to the sluggish performance of low-carbon heating, the amount of investment into energy efficiency and management businesses in 2020 had increased tenfold compared to 2016 (Figure 6). We found around 18 deals per year with an average total yearly investment of £66 million between 2016 and 2020 (the median deal is around £500,000). While energy efficiency and management is trailing the larger investment amounts in businesses related to solar or wind and offshore technologies, this is at a level comparable to the investment into batteries.

Examples of notable recent investments include the online platform Love Energy Savings (£25 million in 2018) and grid balancing company The Faraday Grid (£25 million in 2019) which however later became insolvent. Investments related to insulation include construction materials company SIG (£150 million in 2020) and Q-Bot who have developed an underfloor insulation robot (£7.4 million over several deals since 2016).

Interestingly, the growth in the raised investment amount for energy efficiency and management was preceded by a strong growth in research activity (which is now closer to the stabilising category of our typology). This suggests the possibility that research signals could be a leading indicator of future business investment, which we plan to investigate in upcoming work.

An uncertain future for private investment in low-carbon heating

The investment in energy efficiency and management is a promising sign as these technologies complement heating solutions and help reduce their operational costs. The data for low-carbon heating, however, begs the question as to whether investment in this area might be dormant and why that might be.

In our research project data, we saw several new large research projects in the past two years that integrate heat pumps into wider heating systems. Once the scaled-up projects have proven the value for money of this technology, we might enter a sweet spot and see an increase in private sector investment. It might also be the case that some investment is underway inside established firms, activity which would not appear in the dataset we used.

At the same time, we need to make sure that the existing business environment and business models are conducive to the extensive rollout of low-carbon heating. A recent report by PwC was less than optimistic about the opportunities of attracting capital for residential heating infrastructure, citing issues with scalability and a lack of comprehensive home energy efficiency standards.

The Green Finance Institute has proposed twelve financial solutions that could help overcome investment barriers to decarbonising heating. These include innovative business models such as heat as a service and tools that enable coordination of customers at a local level and help reach a critical mass of demand.

We have technologies to decarbonise household heating, but now need commercial pathways for deploying and scaling them. To achieve this goal, investors, businesses, funders and government should support the development of innovative business and financing models such as heat as a service or schemes that attach cost for heating decarbonisation to home mortgages. This might involve building on test beds such as the Energy Catapult’s Living Lab or ensuring the Heat Pump Ready Programme invests in new business and financial models. The wider economic, policy and social contexts in which heating technologies are developed are as important as the technologies themselves.

For the low-carbon heating sector to flourish and attract future investment the government also needs to create an attractive policy environment. A major barrier to the potential for businesses to operate at scale is the shortage of tradespeople with the right skills. According to a study by EY, there are currently about 1,200 heat pump installers. The Heat Pump Association estimates that this has to increase eightfold to almost 10,000 in order to meet the government’s ambition of 300,000 yearly installations by 2025. Installer shortages were already apparent during the recent short-lived run of the Green Homes Grant scheme. Similarly, the Heat Network Skills Review published by BEIS in 2020 also highlighted the risk to deployment of heat networks if skills-based barriers are not overcome (particularly in key technical roles or project management roles).

There are some promising new initiatives that could help fill these gaps. They include the Retrofit Academy, National Centre for the Decarbonisation of Heat, the Betateach platform to support peer learning between installers and new courses for heat pump installers. Leveraging data-driven approaches to identify transferable skills and support career transitions both within and between sectors could further help overcome skills shortages. Nesta’s Open Jobs Observatory has also made inroads here, through spotting green jobs in online job postings and monitoring how they are spread across the UK, which will be critical for helping workers to transition into these roles.

A further challenge is that the UK low-carbon heating market arguably falls into an investment gap between venture capital and private equity. We already have some fairly well-developed low-carbon heating technologies (such as heat pumps) which may make the sector less attractive to venture capitalists who more commonly support early-stage innovation. The exception may be the novel business and financing models discussed earlier. Private equity investors, on the other hand, are often more focused on scaling, installing and optimising more developed technologies but currently the UK low-carbon heating market is too small to attract this sort of capital.

The threat of the climate crisis and proportion of emissions from UK household heating justifies substantial efforts from the government to prime the market. Once the market has reached sufficient size to become self-sustaining, support can be gradually withdrawn. However, current support is not of sufficient scale: the UK Green Building Council has called the newly announced £5,000 heat pump grant a ‘drop in the ocean’. And previous efforts such as the green homes grant voucher scheme have been criticised for being poorly designed and ending too quickly.

Finally, electricity is currently subject to levies that gas is not, so consumers have less incentive to adopt low-carbon heating, which in turn disincentivises investors and businesses from focusing on low-carbon heating. The government has committed to rebalancing energy prices in its Heat and Building Strategy and this needs to be implemented.

For the low-carbon heating sector to flourish and attract investment in future the policy environment will need to be supportive. To facilitate this, the government should undertake measures such as:

- Tackling skills shortages among installers as there are currently not enough trained people to decarbonise UK heating quickly enough.

- Providing stable, well-designed consumer incentives for low-carbon heating and energy efficiency as current schemes are not substantial enough and previous approaches were too complex and short lived.

- Ensuring commitments to rebalance energy prices are implemented rapidly so that electric heating can compete with gas.

Where is the hype train heading?

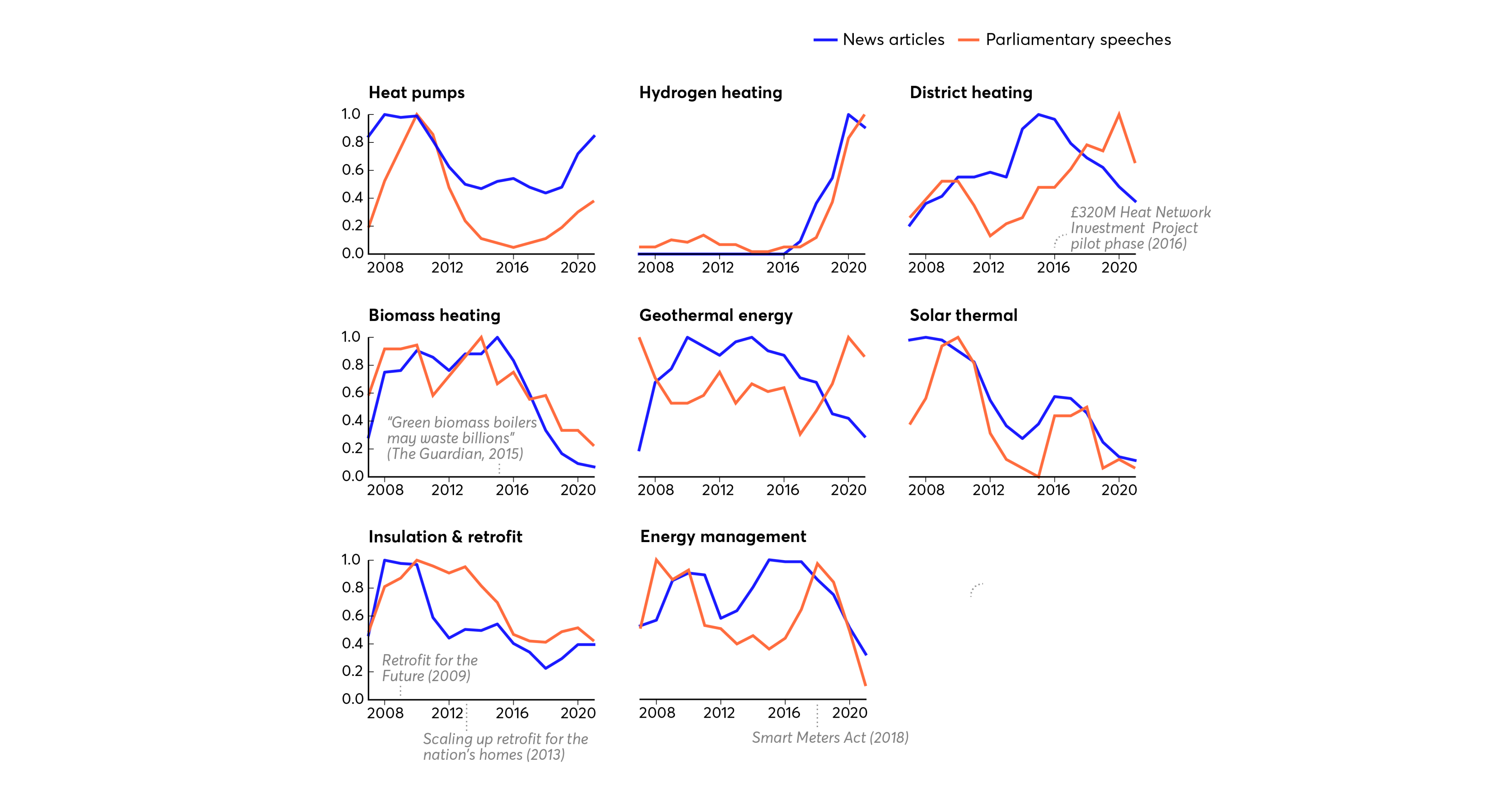

While the public discourse trends exhibit varied patterns for the different types of low-carbon heating and energy efficiency and management technologies, heat pumps and hydrogen heating stand out as having recently exhibited a positive upward dynamic for both The Guardian news coverage and parliamentary mentions (Figure 7).

Figure 7. Increasing references to heat pumps and hydrogen heating in public discourse. Normalised number of articles in The Guardian and Parliamentary speeches mentioning low-carbon heating and energy efficiency and management technologies (three year rolling mean).

Figure 7. Increasing references to heat pumps and hydrogen heating in public discourse. Normalised number of articles in The Guardian and Parliamentary speeches mentioning low-carbon heating and energy efficiency and management technologies (three year rolling mean).

Therefore, we looked in greater detail at the public discourse around these two technologies, and evaluated the patterns in the number of mentions in news and parliament.

Heat pumps approaching the plateau of productivity

News discourse analysis suggests that heat pumps, after an initial wave of hype around 2008, have moved on from a dip in coverage and are now attracting a renewed interest both in the news and parliament (Figure 8).

We find that this pattern bears resemblance to the typical trajectory of expectations around innovations. One example is the widely referenced Gartner® Hype Cycle™. For example, at the ‘peak of inflated expectations’ phase of the Hype Cycle™, Gartner® says that ‘Early publicity produces a number of success stories — often accompanied by scores of failures’ whereas at the ‘trough of disillusionment’ phase Gartner® suggests that ‘Interest wanes as experiments and implementations fail to deliver.’

This pattern also echoes the boom and bust of expectations around renewable energy technologies in the late 2000s and their recent resurgence. However, the share of energy and environment articles in The Guardian that mention heat pumps has increased by about 75 percent between 2016 and 2020, suggesting that the interest in heat pumps is not driven just by these macro trends. The analysis was completed before the release of the recent Heat and Buildings Strategy, which we expect to drive a further increase in the mentions of heat pumps.

While earlier news articles focused on what heat pumps are and how they work, recent discourse appears increasingly centred on the practicalities of adoption, such as costs, government grants, installation issues (eg, there being insufficient number of installers) or problems with operation (eg, issues during cold weather). The share of mentions of the word ‘homes’ together with ‘heat pumps’ have increased about seven times since 2015. Interestingly, air source heat pumps have recently been mentioned more often compared to ground source ones (about twice as often in 2020), perhaps owing to their lower installation costs.

Figure 8. Heat pumps approaching the ‘plateau of productivity’. The number of news articles in The Guardian mentioning heat pumps, which appears to follow the typical evolution of expectations around innovations.

The final stage of the Hype Cycle™ model is the ‘plateau of productivity’ where, as Gartner® suggests, ‘Mainstream adoption starts to take off’. While we are now seeing references to the practical aspects related to adoption in the news discourse, it remains unclear whether the necessary investment is in place to scale up supply.

Figure 8. Heat pumps approaching the ‘plateau of productivity’. The number of news articles in The Guardian mentioning heat pumps, which appears to follow the typical evolution of expectations around innovations.

Figure 8. Heat pumps approaching the ‘plateau of productivity’. The number of news articles in The Guardian mentioning heat pumps, which appears to follow the typical evolution of expectations around innovations.

A wave of hydrogen hype

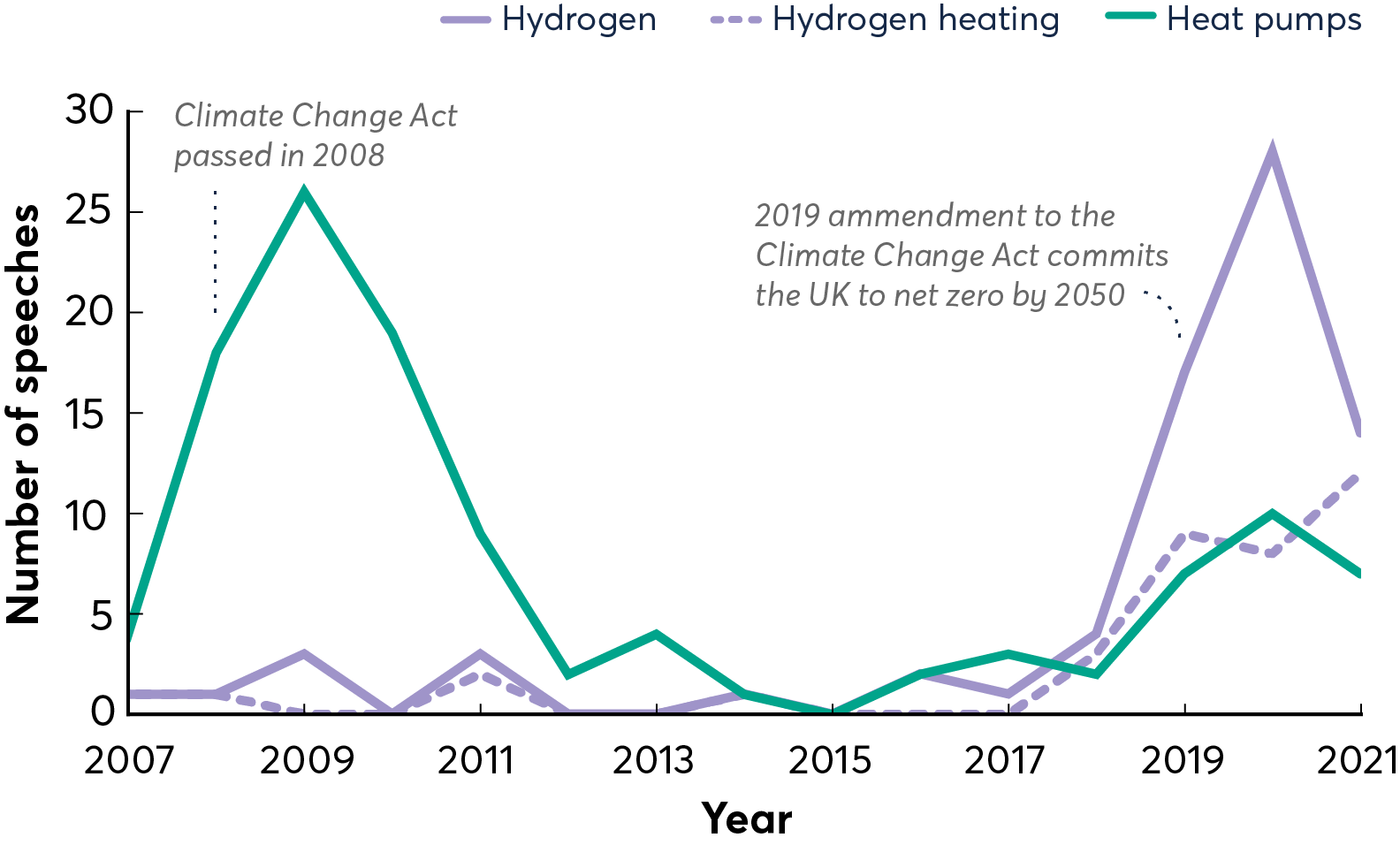

In parliamentary debates, heat pumps are often mentioned as an example together with other low-carbon alternatives – and since 2019, increasingly alongside hydrogen. Indeed, hydrogen heating has recently broken through in the discourse, riding on what appears to be a wave of hype about hydrogen energy (Figure 9).

Figure 9. Hydrogen on the policy agenda. Number of speeches made in the House of Commons, which mention hydrogen, hydrogen heating or heat pumps (based on analysis of Hansard data)

There were five times as many news articles about hydrogen in The Guardian in 2020 compared to 2016, and mentions of hydrogen heating have increased twofold since 2017 when hydrogen boilers were first featured in the news (Figure 10). Before that, hydrogen was mostly mentioned in the context of transportation, but the co-locations of terms ‘hydrogen’ and ‘cars’ in the same sentence have now decreased to about half the level of 2010.

Figure 10. A wave of hydrogen hype? Proportion of The Guardian UK articles on environment and energy that mention hydrogen, hydrogen heating or heat pumps.

The content of news discourse appears to be less about practicalities and more about first technology demonstrations (eg, zero-carbon hydrogen was injected into gas grid for first time in 2020) or debates on the general advantages and disadvantages of hydrogen energy (eg, hydrogen being called a “central part of government’s plan” versus “a dangerous distraction”)

Figure 9. Hydrogen on the policy agenda. Number of speeches made in the House of Commons, which mention hydrogen, hydrogen heating or heat pumps (based on analysis of Hansard data)

Figure 9. Hydrogen on the policy agenda. Number of speeches made in the House of Commons, which mention hydrogen, hydrogen heating or heat pumps (based on analysis of Hansard data)

Figure 10. A wave of hydrogen hype? Proportion of The Guardian UK articles on environment and energy that mention hydrogen, hydrogen heating or heat pumps.

Figure 10. A wave of hydrogen hype? Proportion of The Guardian UK articles on environment and energy that mention hydrogen, hydrogen heating or heat pumps.

A report by Oxford Institute of Energy Studies from last year has evaluated that while hydrogen will certainly play a role in decarbonisation of the energy system – especially when it comes to industrial applications – it will be particularly challenging to use it for decarbonising residential space heating. In part, this is due to the need to adapt the existing natural gas infrastructure to work with 100 percent hydrogen gas, as well as the challenge of scaling up the production of sustainable ‘green’ hydrogen. Other experts express similar concerns about the potential of hydrogen for heating.

According to our typology, research on hydrogen heating appears to be in the emerging category. However, we have identified a rise in discourse about the so-called hydrogen economy, alongside the presence of strong institutional lobby groups. This suggests that it is important to consider the future consequences of building hype around the applications of this technology. For example, there is a possibility that consumers and investors will wait to see if the hydrogen economy matures instead of pursuing alternatives such as heat pumps that are more viable in the short term. This could put decarbonisation goals at risk if, as many studies suggest, hydrogen does not ultimately emerge as a viable means to provide home heating at scale.

Consumers should not be distracted from adopting more mature technologies (such as heat pumps) to decarbonise their homes by what appears to be early-stage hype around hydrogen heating.

Conclusions

A more complete picture

The assessment of different signals about research, investment and public discourse has helped us build a more multi-dimensional picture of the technologies involved in decarbonising heating and how they compare with other green technologies.

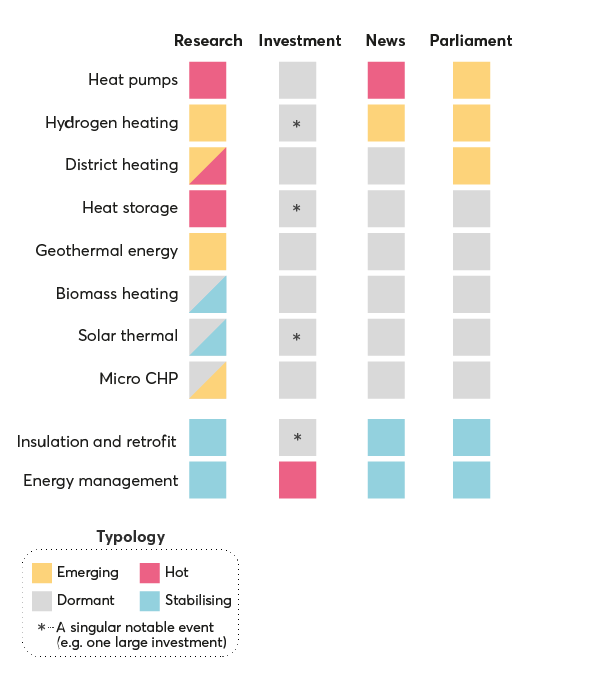

We have characterised signals from each dataset independently and subsequently evaluated the uncovered trends across the sources. We have visualised this as a data-informed heat map (Figure 11), which provides a qualitative perspective of the trends across the different technologies explored through these different datasets.

While low-carbon heating also appears to be backed by substantial research support we find indications that this is not complemented by an equally significant influx of private investment. We have proposed avenues to explore the potential barriers to investment in this area. Meanwhile, in terms of news and policy discourse we do find a momentum around heat pumps and hydrogen heating, whereas district heating, heat storage and geothermal energy appear to be attracting less interest.

In contrast, solutions for energy efficiency and management (and particularly energy management) might be approaching a tipping point, with strong performance in terms of research funding and particularly high growth in investment raised. To make a significant impact, public awareness and adoption of these technologies will need to follow on from research and investment.

We note that Figure 11 reflects a combination of data and judgment by the researcher. Ambiguity is indicated by partial colouring, which might arise if the trends are transitioning between different stages of the typology or if multiple signals (eg, the number of research projects and the amount of research funding) exhibit different trends.

We will continue refining our methodology to aggregate signals quantitatively and to identify potential relationships between the different signals. Going forward, this analysis could also be complemented with sales figures where possible, to build a more detailed picture of adoption trends. As this model evolves, we envisage that this type of heat map could, in future, help to identify innovation opportunities and stagnation across different kinds of social challenges or missions, and Nesta’s Discovery Hub will continue to explore the application of the methodology to different contexts.

Figure 11. Heat map of technology trends for decarbonising heating. An overview of data-informed qualitative UK trends between 2016 and 2020, based on the Innovation Sweet Spots approach.

Figure 11. Heat map of technology trends for decarbonising heating. An overview of data-informed qualitative UK trends between 2016 and 2020, based on the Innovation Sweet Spots approach.

Figure 11. Heat map of technology trends for decarbonising heating. An overview of data-informed qualitative UK trends between 2016 and 2020, based on the Innovation Sweet Spots approach.

A fair heating transition

As we embark on the challenge of decarbonising residential heating, innovation offers many potential pathways to a more sustainable system. However, the technologies we adopt and the way we deploy them could either exacerbate or reduce existing inequalities. Nowhere is this more apparent than in the case of household heating – fuel poverty and cold homes continue to be an acute problem in the UK (every year fuel poverty kills more than 3000 people, and cold homes cause as many deaths as breast or prostate cancer).

The Net Zero Research and Innovation Framework has mentioned improved energy efficiency and flexible demand technologies as ways of helping tackle fuel poverty. In the Gateway to Research data, we found low-carbon heating and energy efficiency and management projects that specifically mention fuel poverty in their abstracts (about five percent in total). For example, the development of an energy efficiency investment optimisation dashboard for social landlords, or new business models for community energy generation (see Climate Positive and CEGADS). We are also able to find businesses (albeit a smaller fraction) that have mentioned fuel poverty in their Crunchbase profile (for example, the geothermal energy company GT Energy, or energy efficiency and management companies Switchee and UNO Energy).

Given that about 13 percent of English households are in fuel poverty there is a strong case for the government to prioritise innovation targeted at tackling this issue. The government should elevate a fair heating transition to the status of a challenge in the Net Zero Research and Innovation Framework, and actively pursue that agenda across all types of heating innovation. The data-driven horizon scanning and innovation mapping methods used in this pilot could then be leveraged to track the progress against this challenge.

Acknowledgements

We would like to thank the following people for their valuable insights and advice that have informed this work. Please note that their input does not necessarily imply endorsement of the conclusions or findings.

- Meredith Annex (BloombergNEF)

- Anton Arts (SET Ventures)

- Simone Boekelaar (Innovate UK)

- Steffen Boehm (Itonics)

- Bryony Butland (UKRI)

- Claire Curry (BloombergNEF)

- Craig Douglas (World Fund)

- Connor Duffy (Clean Growth Fund)

- Paul Egan (Founders Factory)

- Claire Hamer (Planning Inspectorate)

- Joel Herzig (UKRI)

- Carl Holland (Energy Systems Catapult)

- Greg Jackson (Octopus Energy)

- Professor Gary Kass (Centre for Environment and Sustainability, University of Surrey)

- Douglas Morrison (Construction Scotland Innovation Centre)

- Alexei Mulko (UKRI)

- Olamide Oguntoye (Tony Blair Institute for Global Change)

- Gladino Pedron (Envisioning)

- Stephen Price (Clean Growth Fund)

- Professor Daniele Rotolo (SPRU, University of Sussex Business School & Polytechnic University of Bari)

- John Rowland (White Lake)

- Karl Sample (Energy Systems Catapult)

- Suzanna Sia (Johns Hopkins University)

- Andrew Symes (IP Group)

- Benny Talbot (Community Energy Scotland)

- Charlie Warwick (GO Science)

- Jonathan Wentworth (POST)

- Michell Zappa (Envisioning)

Editor: Siobhan Chan

Public discourse analysis: Jyldyz Djumalieva

GARTNER and HYPE CYCLE are a registered trademark and service mark of Gartner, Inc. and/or its affiliates in the U.S. and internationally and are used herein with permission