Innovation Sweet Spots: digital technologies for the early years

Executive summary

Our study points to a building wave of research, products, services and companies aimed at supporting the development of children aged 0-5, and innovation in digital technologies is powering this wave. Our analysis of large datasets has found that between 2019-2023, research funding awarded by UK Research and Innovation (UKRI) for early-years digital technologies increased by 166%, while global research publications on this topic rose by 78%.

However, despite encouraging signals and fast-paced innovation, this ecosystem will need firmer foundations in future. For example, there are likely to be limited resources in the early-years sector to trial these products. In addition, a lack of reliable evidence around efficacy and safety could give parents reason to mistrust new technology.

Sectors as diverse as health and defence have been preparing for years for the seismic shifts predicted to flow from AI-enabled digital transformation. Yet, comparatively, the question of how these tools could be harnessed in the service of families and children has received barely any attention. While there has been some analysis of digital technologies and education, the focus has often been on the ‘edtech’ market for older children and adult learners rather than on the early years.

Given what we know about the importance of early intervention and the emerging capabilities of AI and digital technologies, we need to empower policymakers, parents and early-years practitioners to maximise the potential of this wave of innovation.

Introduction

In the UK, too many young children don't get what they need to develop and thrive in the early years. Through our fairer start mission, Nesta is seeking to tackle this. In this report we consider the emergence of a wave of AI and other digital technologies aiming to support the early-years sector and parents to better detect and manage child development needs.

While traditional methods for assessing child development (such as the Ages and Stages Questionnaires) are predominantly low-tech and have limitations in terms of accuracy and timeliness, our study points to a burgeoning innovation ecosystem of digital technologies and advances in AI that could enhance the way we detect issues and support child development. For example, AI-powered speech recognition has demonstrated promise in the early detection of dyslexia, and AI could be used to support speech and language therapists to help more children. More generally, new advances in generative AI have the potential to have an impact on the early years by supporting some of the core tasks associated with teaching and parenting such as designing activities, easing the administrative burden, or promoting shared reading.

Here we examine trends in these fields and begin to explore how to overcome challenges in integrating these innovations into practice. This study is part of Nesta’s developing programme of work to harness digital technologies in early childhood, which will include prototyping with users.

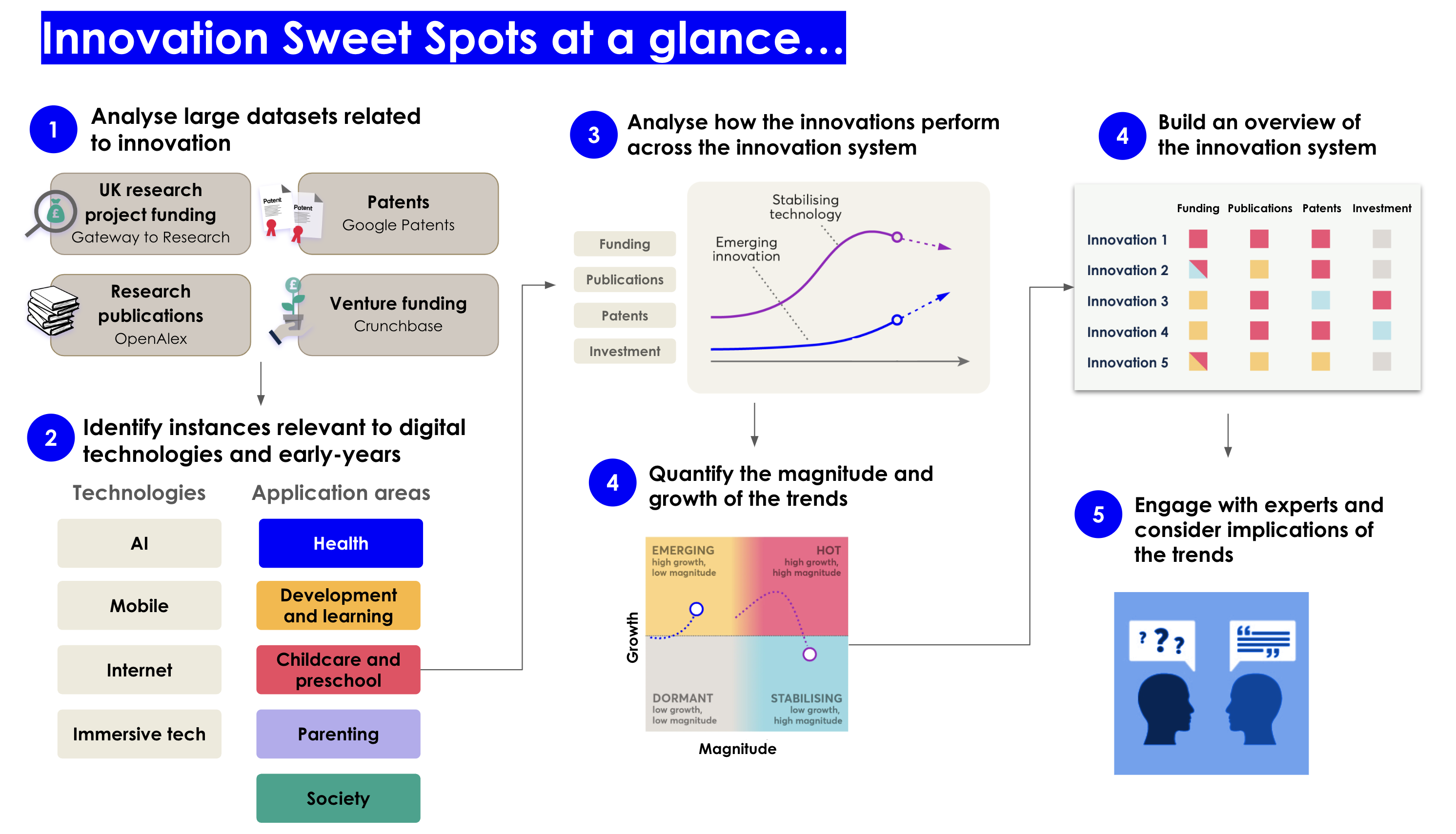

Searching for Innovation Sweet Spots

Using our Innovation Sweet Spots methodology, we analysed datasets featuring tens of thousands of research projects, publications, patents and companies to map trends around digital technologies aimed at supporting the development needs of children aged 0-5. We identified applications using AI and data analytics, mobile technologies, the internet and ‘immersive technologies’ such as augmented reality, robotics and wearables. We then mapped the areas where these technologies are applied, including health, development and learning, parenting, childcare, family income and the labour market.

Our datasets cover global research publications, venture funding and patenting activity as well as UK research funding trends, capturing a rich view of the innovation system of early-years digital technologies. To our knowledge, this is the first time that innovation trends in this sector have been mapped using such a diverse array of data sources. Most other analyses tend to focus on the edtech market as a whole.

Alongside this quantitative analysis, we considered the implications of our findings with a range of early-years sector experts, and brought together a small focus group of parents to explore how some of the identified innovations might be perceived by caregivers.

Figure 1. Innovation Sweet Spots at a glance

Figure 1. Innovation Sweet Spots at a glance

A wave of AI and digital tech innovation in early years

Our analysis reveals a highly dynamic innovation ecosystem around early-years digital technologies in the UK and worldwide.

There is particularly strong growth ‘upstream’ in research and development, with a 166% increase in research funding awarded by the UKRI between 2019-2023, totalling almost £60 million in new funding during this time period. The largest contributor to this funding (36%) is the Medical Research Council, which has an area of investment directly related to early childhood development. At the same time, the number of research publications in this area increased by about 78% globally, with at least 2,500 new publications. Both the funding and publication growth figures are considerably higher than the corresponding baseline growth estimates across all research fields taken together, which we estimate to have remained largely static (Figure 2).

Figure 2. Growing wave of early-years digital technologies

Institutions based in the United States are leading by contributing around 28% of the total publications, while the UK leads in Europe with around 9% of the total publications (which is higher than the UK contribution to the global publication output of 5.9% across all sectors).

These trends indicate growing interest in early-years digital technologies by researchers both globally and here in the UK. The publications range from medical research, such as the University of Oxford’s project on using AI to assess foetal wellbeing, to Manchester Metropolitan University’s investigation of the role of digital technologies in language and literacy learning. The growth of early-years digital technologies also outperforms publication output concerned with broader edtech topics covering all levels of education, which we estimate to have increased by 49% in 2019-2023 (with around 29,000 new publications in this period).

Notably, however, UK research funding data suggests there is somewhat limited support or scope for the commercialisation of early-years innovations. Innovate UK, which is part of UKRI and specialises in helping businesses grow through the development and commercialisation of new products, processes, and services, awarded only around 10% of the UKRI funding related to early-years digital technologies. As a baseline comparison, Innovate UK contributes to around 20% of total UKRI project funding across all fields of research. While the percentage for early-years digital technologies increases to about 17% when excluding health-related projects, it is still lower than for other sectors we have researched previously, such as low-carbon heating technologies and food technologies, where Innovate UK has provided around half of the research funding.

Slower, but still positive, growth ‘downstream’ in market-ready applications

The growth of patenting activity and venture funding – indicators of downstream innovation that is closer to commercialisation and market impact – has been positive, albeit comparatively slower than the baseline growth across all sectors (see Figure 2).

Patent applications for early-years digital technologies have risen by 20% globally when excluding patents from China. Including China’s patents, the growth rate is close to zero. We report both growth estimates as China dominates in terms of the number of patents. However, recent regulatory changes may have hindered the growth of the edtech market in China, masking growing patenting activity elsewhere. Other countries with larger patent application counts include Korea, the US and Japan, while the UK does not feature prominently in the patent data.

Global venture funding for early-years digital technology start-ups peaked during the pandemic (Figure 3), fuelled by low interest rates and a surge in the direct-to-consumer business model to meet rising demand from parents for educational tools. We estimate investment grew at around 41% between 2019 and 2023, reaching a total investment of around £4.2 billion during this period.

Figure 3. Venture funding into early-years digital technologies spiked during the pandemic

Several US-based companies secured particularly sizeable funding rounds in 2021. Notable examples of the large deals during the pandemic include Jam City, developer of mobile games for children and adults, which raised £254 million, and PatPat (an e-commerce platform for clothing for baby and children), which secured £371 million. Investments with more relevance to supporting early-years development included the educational app LingoKids (£28 million) and childcare management software companies such as Lillio (formerly HiMama) and Brightwheel raising £41 million and £40 million respectively.

When excluding the handful of large deals (greater than £100 million), we find that the investment growth is more modest at 3.3% in 2019-2023, reflecting the challenging market conditions of recent years. The path to market for early-years products and services is now complicated by higher interest rates increasing the cost of financing ventures, as well as the cost-of-living crisis and acute funding constraints for nurseries, which limits their buying power when it comes to new services. There are, however, signs of potential recovery with the investment in 2023 being slightly higher compared to 2022 (particularly in the European early-years market).

In Europe, the UK is at the forefront of the field with nearly £185 million invested in 2019-2023. However, the UK is still behind the US (which leads the world at £2.6 billion), India and China. Overall, while early-years investment figures are comparatively modest compared to the broader edtech sector's £32.9 billion raised in 2019-2023 (covering all levels of education), this represents a significant increase from a decade ago and the growth has been slightly higher than the overall edtech investment (which showed 34% growth during the same period).

Digital technologies are central to commercialisation

Some of the overall early-years research funding, publications, patents and venture funding we analysed is directly linked to digital technologies, while the rest concerns other forms of research and development such as studies of health issues of young children, projects on early-years interventions or patents concerning physical hardware innovations.

We found that venture funding is more frequently associated with digital technologies compared to UK research funding, research publications or patents. This suggests that the role of AI and other digital technologies becomes more significant for early-years innovation as it gets closer to commercialisation and market impact (Figure 4).

We estimate only around 6% of research publications related to early years are associated with digital technologies, whereas about 20% of early-years research funding awarded by UKRI, 18% of patent applications and 56% of venture funding is associated with digital technologies. The comparatively low percentage of research publications suggests that, despite the recent growth, there might still be a gap in terms of evidence on digital technology interventions in the early-years context.

Figure 4. Larger role of digital technologies in innovation closer to commercialisation

AI is becoming increasingly prominent among early-years digital technologies

A substantial proportion of early-years digital technology innovation is already associated with AI and data analytics: approximately two-thirds of newly awarded UK research funding (68%) and global patents (63%) in 2019-2023, as well as about 15% of early-years digital technology venture funding (Figure 5). We also find high growth rates for AI-related early-years innovation, with research funding increasing by 148%, research publication output by 91% and venture funding by 74%.

Looking forward, AI applications for early years are set to expand even further. Generative AI tools such as large language models (LLMs), which can generate high-quality text, have a wide range of potential applications in early years and are expected to become ever more advanced and well-funded. The global market saw around £23 billion invested in companies developing generative AI technologies for all sectors in 2023 alone. Generative AI is already being used in early-years contexts: examples include a nursery software assistant for writing updates for parents and staff, drafting assessments and two-year checks as well as creating stories and promoting shared reading.

Figure 5. AI is becoming increasingly prominent in early-years digital technology innovation

How are digital technologies applied in early years?

To better understand how digital technologies are being targeted towards child development needs, we distinguished between several application areas: health, development and learning, parenting, childcare and preschool as well as society (a broad category concerned with family income, labour market, social services, peer-to-peer interactions and reducing inequalities).

We identified instances in our innovation datasets where these areas were mentioned together with digital technologies. In this way, we can estimate where the potential of digital technology is being explored most intensively.

Our analysis shows that there is a strong focus on health applications, with around two-thirds (68%) of UK research funding awarded for early-years digital technologies, and 36% of global research publications and 35% of patent applications being associated with this application area (Figure 6).

Only venture funding exhibited a different trend, with most early-years digital technology start-up funding being associated with the development and learning category (34.5%) – although a substantial proportion of funding was also raised by health-related start-ups (14.7%).

Figure 6. Early-years digital tech is most likely to focus on health, followed by development and learning

Based on the datasets, we have identified a key trend to watch for in each of our areas of application. The examples we highlight are illustrative of future potential, but in many cases further development and validation will be needed before they begin to deliver wider benefits.

Trend to watch in health: predictive early intervention

Our data analysis surfaced several cutting-edge tools aiming to identify or predict potential health problems at an early stage. One example is advanced electronic foetal monitoring, which harnesses AI to predict and track the health of a foetus during pregnancy. This technology aims to identify the early signs of an inadequate supply of oxygen to the foetus so that medical practitioners can intervene sooner, potentially preventing brain damage and developmental delays. Similarly, we have found examples of trialling AI to forecast health outcomes in very premature babies and using children’s hospital health records to predict childhood obesity. These open up the potential of more targeted early support, moving from a reactive approach to a model that proactively addresses issues before they have a detrimental impact on child health.

Trend to watch in development and learning: accessible personalised support

We identified a trend toward personalised development and learning support, often through the use of mobile devices. Recent research suggests that matching the speed of information delivery to an individual's natural brain rhythms can help children learn faster. Mobile apps that use AI eye-tracking technology, such as Temporeading and Braingaze, claim to personalise the learning experience for children based on such neurocognitive research, potentially aiding neurodivergent children. Other neurocognitive games, such as EarlyBird, aim to assess literacy and screen for dyslexia, helping schools and parents detect issues and providing tailored instructional resources.

We also found examples of developers using machine learning to track infant wellbeing and emotional development. For instance, ChatterBaby claims that its app can help parents decipher the meaning behind their baby's cries and respond appropriately, with research showing some success for the algorithm in distinguishing between hunger, fatigue and pain.

Trend to watch in parenting: enhancing the quality of interaction

We found that many technologies intended to support parenting are focused on improving parent-child interactions through technology-mediated scaffolding, providing parents with practical prompts and suggestions to enhance their engagement. For instance, platforms such as EasyPeasy provide personalised learning activities for parents, with research showing that low-income families using the app saw improvements in their children’s cognitive self-regulation. The platform Tandem (currently working in partnership with Nesta) supports shared reading experiences by using AI for interactive sessions and co-creating storybooks. Despite concerns from some quarters that excessive digital technology use by parents might reduce interaction, this next wave of tools aims to take a more sophisticated approach to facilitating engaging interactions between caregivers and children.

Trend to watch in childcare and preschool: virtual integration and communication

A number of the innovations we found in the area of pre-school and childcare focus on building networks between those involved in early-years education. Streamlining communication between parents has the potential to reduce administrative workload for nursery practitioners and childminders. Providers such as Kindiedays share best practice in pedagogy among early-years practitioners.

Childcare platforms offer a wide range of services, such as Koru Kids, which matches parents with nannies; Famly, which provides nursery management software; and Illumine, which supports early-years practitioners to communicate with parents about their child’s progress.

Trend to watch in society: community and communication

One development we observed in the society category sees digital technology being used to analyse and improve local environments. For instance, nine US cities used Google Street View to evaluate preschool neighbourhoods and assess whether community features such as outdoor play facilities and safety impacted young children’s developmental outcomes.

Other examples in the society category include online communities such as Peanut, where people can connect on topics such as fertility and motherhood, as well as software that helps manage family finances and streamline foster care and adoption services.

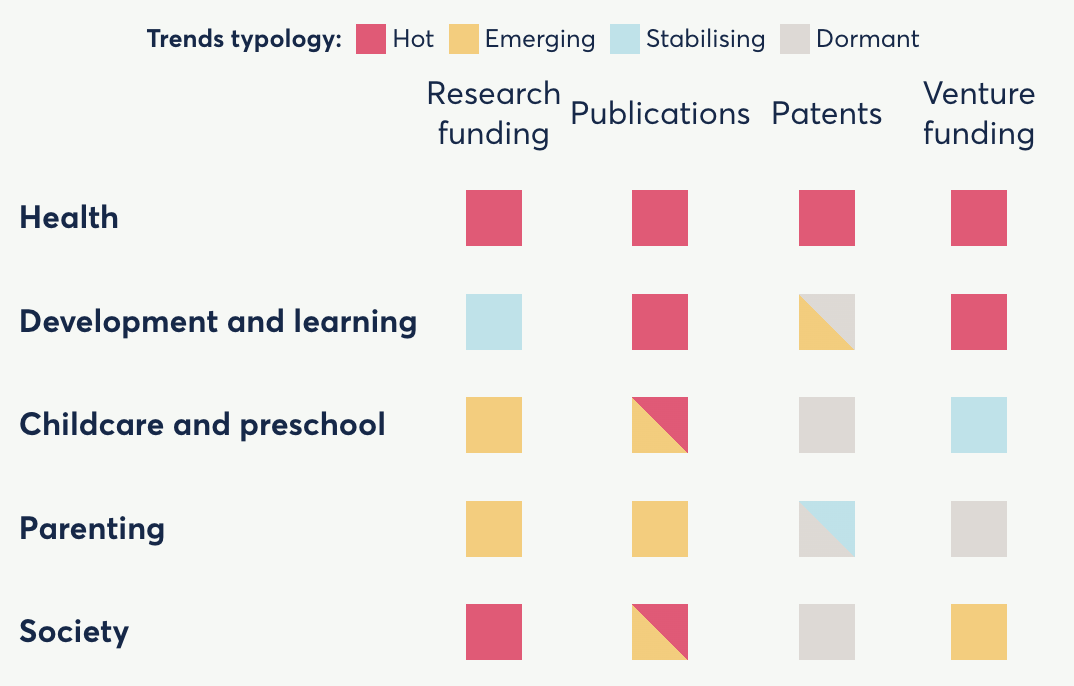

Overview of early-years digital technology application trends

We have summarised our analysis of early-years digital technology application trends across our datasets in the heat map below (Figure 7). It takes into account the growth and magnitude (so, the average level of research and venture funding or patent and publication counts) of innovation activity in 2019-2023 across the different datasets.

For example, the ‘parenting’ application is categorised as ‘emerging’ when it comes to research funding and research publication output – with positive growth but relatively lower magnitude – but comparatively ‘dormant’ when it comes to venture funding (so, negative growth and small magnitude). This suggests that there could be a gap when it comes to the commercialisation of innovations directly supporting parenting behaviours.

In contrast, areas such as ‘health’ and ‘development and learning’ are ‘hot’ in terms of research publication output as well as venture funding (relatively high growth and high magnitude), suggesting a particularly dynamic innovation ecosystem around these areas. Finally, some areas can be seen as 'stabilising’ with very low or negative recent growth but substantial magnitude, such as research funding for ‘development and learning’ or venture funding for ‘childcare and preschool’, which might indicate a maturing of the innovation activity in these areas.

UK research funding, global research publishing, patenting and venture funding in 2019-2023

Figure 7. Heat map of digital technology application trends in early years

Riding the wave: tapping into the benefits of early years innovation

To realise the full potential of digital technologies for young children, their parents and early-years practitioners, we need a functioning innovation ecosystem providing the conditions for the best tools and services to grow sustainably. As our research shows, a number of the building blocks are clearly in place: UK research funding and publications focused on innovations in this field have grown substantially over the last five years, and we can see promising examples of companies taking products to market. As is often the case with a boom in technological innovations, many of these will no doubt fail, but a select few might just move the needle.

However, before that can happen, we need a deeper understanding of the challenges and barriers limiting the potential for growth and social impact. From the data analysis and case study evidence we have gathered, and from testing these findings with experts and parents, several consistent themes emerge. While our research does not delve deeply into solutions for these challenges, it highlights some promising directions for further exploration.

Addressing evidence gaps with systematic evaluation

The experts we interviewed suggested that more evidence is needed about how AI and digital tech projects can boost children's outcomes. A lack of reliable evaluations led some of the early-years practitioners and parents we interviewed to express concerns about quality, standards and possible negative impacts on child development from these technologies.

Addressing these concerns means generating robust evidence on the efficacy and safety of early-years innovations to build users’ confidence. This requires, as Nesta has outlined in earlier research, a stronger research infrastructure for systematic testing. More resources need to be directed toward rigorous evaluations that strengthen the evidence base around early-years digital technologies. When undertaking such evidence gathering, lessons might be learned from Education Endowment Fund-funded evaluations, which use an independent panel of evaluators and assess educational interventions through rigorous approaches such as randomised trials in schools.

Designing and testing tools with caregivers

We discussed AI and digital technologies applications with a small number of parents, many of whom expressed mixed feelings about the technology. While potential benefits were recognised, some feared that using AI might cause them to second-guess their instincts and reduce their sense of control. They also wanted greater transparency from developers about how AI was being integrated, as well as the limitations, especially in health-related applications, which our research shows makes up a large part of early-years digital technology. Although some parents viewed AI more positively for providing tailored support and resources, particularly for children with special needs, concerns about safety and cost – potentially exacerbating educational inequalities – tempered their optimism.

Greater parental and caregiver involvement in early-years digital technology development could go some way to engaging with these concerns. Early insights from Nesta's work on generative AI to promote reading in families indicates that parents and caregivers can become more open to using this technology if they experience the benefits in practice. Understandably, it can be hard to conceptualise the benefits and risks of these innovations in the abstract. Trying them out in a controlled and responsible way with continuous feedback from parents and caregivers can address concerns and also help developers sharpen their value proposition. One way to catalyse this would be to explore the use of a testbed where practical applications can be trialled and shared in real-world settings with parents and caregivers. (For inspiration, see this 2019 Nesta-run testbed for edtech.)

Addressing barriers to commercialisation

The experts we shared our findings with observed that the lack of specific regulations for early-years technology, coupled with the recent cost-of-living crisis, is influencing investors’ appetite for risk when it comes to early-years digital technologies. This is reducing support for start-ups in the early-years sector. The market for early-years technology has also become increasingly unstable, exacerbated by funding shortages in nurseries and a significant downturn in the parental consumer market since Covid-19. Our research also shows relatively modest funding from Innovate UK being directed to early-years technologies when compared to other domains we have investigated. This suggests barriers to commercialisation for these technologies.

A clearer regulatory and assessment framework for early-years technologies (similar to that for health tech) could improve confidence among consumers, while also reassuring investors about the long-term viability of the market. Given the field is so fast-moving, there is a case to explore whether such regulations might take an anticipatory approach, emphasising flexibility, collaboration and innovation.

Realising the potential of early-years innovation

Digital innovations and AI in sectors such as health and defence have recently received considerable attention and are high on political agendas. But the infrastructure for deploying these technologies in early-years settings remains neglected. Stronger foundations for early-years tech are clearly needed for the potential of this wave of innovation to be fully realised. On the policy horizon, there are promising opportunities such as the new AI Opportunities Unit, to be set up in the heart of the UK Government, which could allow us to start looking towards the social impact of these technologies in underserved fields such as early years.

Over the coming months, Nesta will explore how AI can empower early-years professionals to provide more high-quality and effective early education experiences, alongside continuing to invest in promising companies.

Acknowledgements

We would like to thank the following people for their valuable insights and advice that have informed this work. Please note that their input does not necessarily imply endorsement of the findings or conclusions:

- Professor Jenny Gibson, University of Cambridge

- Dr Laura Outhwaite, University College London

- Liz Hodgman, Local Government Association

We thank the parents and caregivers who participated in our focus group discussions.

We thank Celia Hannon for her support and leadership for the Innovation Sweet Spots project. We are also grateful to our colleagues Tom Symons, Sarah Cattan, Umesh Pandya, Ishaan Chilkoti and Lisa Barclay for their insightful reflections and feedback on this work. We thank Solomon Yu for his help with data engineering.

Editor: Siobhan Chan

Illustrator: Eva Bee

Methodology overview

The following section provides an overview of our data-driven approach to analysing innovation trends. In addition to the quantitative analysis, we also engaged with a small focus group of parents (n=9) to consider how some of the innovations might be perceived by caregivers.

Datasets

We sourced research funding data from the Gateway to Research portal on research projects funded by UK Research and Innovation (UKRI). UKRI is responsible for funding a large proportion of UK research and development (£6.2 billion, or about 38% of the UK Government’s R&D expenditure in 2022).

Research publication data was collected from OpenAlex, an open-source database of around 258 million publications. Patents were collected from the Google Patents database, which includes more than 120 million patent publications from more than 100 patent offices. Venture capital investment data was sourced using Crunchbase, which is a business information database covering around 3.4 million start-ups and companies. All three of these datasets have a global coverage.

We collected and applied our analysis methods (described below) to the entire Crunchbase and Gateway to Research portal datasets. For OpenAlex and Google Patent data, we first collected representative subsets using a set of keyword searches related to early-years context. Due to this data collection approach, we note that our absolute number of publications or patents are likely underestimated.

Regarding patents, we note that contributions from the UK and other European countries might be partially masked by the patent applications filed with the European Patent Office or World Intellectual Property Organization. Moreover, UK-based innovation might be more focused on services and software, which can be harder to patent, whereas patents in our sample often involved some hardware component.

When reporting venture funding trends, we considered relatively early stage funding rounds, which are usually associated with start-ups, such as angel, seed, and all types of series funding up to series E (inclusive). We do not include funding associated with more mature companies such as mergers, buyouts, debt financing and initial public offerings (IPOs) or post-IPO funding.

Identifying data relevant to early years

We used supervised machine learning to identify instances of research projects, publications, patents and ventures strictly relevant to the early-years context (concerning children of age 0-5). We manually reviewed and labelled around 150 instances of data in terms of whether it was relevant or not. We then leveraged a large language model (GPT-4 from OpenAI) and prompt engineering to automatically label around 4,800 additional documents, using manual labels as a benchmark for the accuracy of the labelling. We fine-tuned a pre-trained deep learning model (DistilBERT) using the manually and automatically labelled data for binary classification of relevant vs not-relevant documents with accuracy around 90%.

Our filtered dataset of relevant instances of data included: 1,085 research projects funded by the UKRI in 2013-2023; 69,748 research publications published in 2017-2023; 25,972 patent applications submitted in 2013-2023; and 9,709 companies with 2,540 funding rounds raised in 2013-2023 (note that not every company has reported funding rounds).

Categorising data in terms of technologies and application areas

We then used a combination of supervised machine learning and keyword search to tag the datasets with granular digital technology and application area categories (32 categories in total). We manually labelled around 50 samples for each granular category and similarly used a large language model (GPT-3.5-turbo from Open AI) to label around 500-1,000 additional documents depending on the category. We then trained an ensemble of five simple classifiers for each category (support vector machine, stochastic gradient descent, random forest, k-nearest neighbours, and logistic regression classifiers) using vectorised document text as features (all-MiniLM-L6-v2 embeddings) – and only accepting results where all five classifiers agreed.

To improve the precision of the categorisation, we also added a keyword filtering step by selecting specific keywords to each category, and performed partial manual review. For the final results, we report the results for the broader, aggregated categories, namely four major digital technologies (AI, Mobile, Internet and Immersive tech) and five major application areas (Health, Development and learning, Childcare and preschool, Parenting, Society). We estimate a precision metric for the major categories between 0.8 and 0.9 depending on the category.

Descriptive analysis

When reporting growth figures, we smooth out the year-to-year fluctuations of a time series (for example, publication counts or venture funding over time) by calculating a three-year rolling mean (moving average) up to 2023. To capture the growth of the time series between 2019 and 2023, we calculate the percentage increase of the smoothed values in 2023 versus 2019. Therefore, the reported growth in the time period 2019-2023 results from comparing the mean across 2017 and 2019 versus the mean across 2021 and 2023. In this way, the growth percentage estimate captures a smoothed growth trend across the past five years.

Caveats

Our datasets have limitations (such as gaps in the coverage of private R&D spending) and the semi-automated nature of our data labelling approach can result in occasional false positive or false negative results. Moreover, our method identifies likely associations between different topics (such as technologies and areas of development and learning) but the nature of the topic associations can vary from strong to circumstantial: for example, a technology might be the focus of a research project or, alternatively, used as part of a research project but not necessarily the primary focus. Due to these caveats, we view our findings as data-informed hypotheses about the innovation system rather than a definitive picture.

The data analysis code is available on our GitHub and more information about the methodology, as well as supplementary figures, can be found in the technical appendix.